A new chapter has been started in the ongoing saga of Vista Outdoor’s sale process. Vista seems to firmly want to sell their Sporting Products division to CSG and take Revelyst (where Camp Chef sits) public, but MNC Capital is determined to not let that happen.

MNC has once again upped their offer, to now over $3 billion, and contends that it’s a much better offer than CSG’s. We may be reading into it a little, but from the press release that MNC put out about the updated offer, things are starting to sound more contentious.

MNC believes that absent its interest in an acquisition, Vista’s share price would trade back to where it was prior to MNC’s initial offer, which was below $30.00 per share. This is evidenced by Vista’s share price decline of 3% or $1.00 per share following Vista Board’s rejection on May 28, 2024 of MNC’s prior proposal. From May 17 until May 28, Vista not only failed to provide needed due diligence, it also did not respond to the merger agreement that MNC had sent the Company.

MNC Capital Letter from June 6th, 2024

Through the whole process Vista has contended that MNC’s offer doesn’t value Revelyst high enough and that the offer has financing contingencies. MNC keeps coming back and saying that neither point is true.

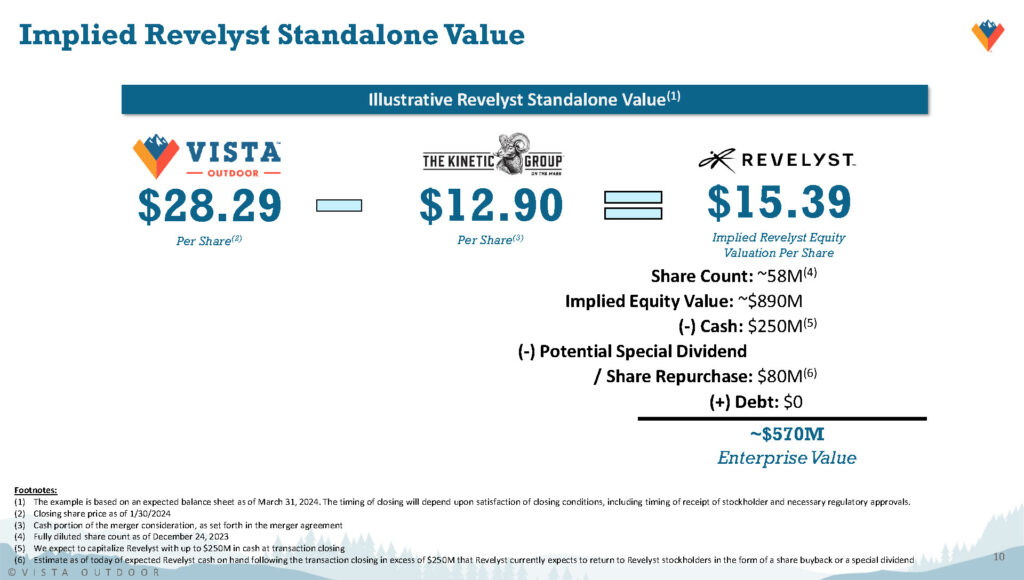

Additionally, the latest offer implies a value for Revelyst of over $1 billion, as compared to Vista’s valuation for Revelyst of $570 million disclosed in its own investor presentation on February 1, 2024.

MNC Capital Letter from June 6th, 2024

MNC is referencing the slides below from Vista Outdoor’s February presentation. In our opinion, it’s a little inaccurate to say that.

{kind=link}

As you can see, part of the enterprise valuation calculation was based on using the cash proceeds from the sale of their Sporting Products division. Changing the transaction also changes the enterprise value with this calculation.

The implied equity value is $890 million at the time of sale, when it would have no debt. That’s a better proxy for the value of the company. Enterprise values in general though aren’t aligned dollar for dollar with what a company would fetch through an acquisition.

It’s also a valuation from the balance sheet at the end of March, and doesn’t have future earnings from growth baked in. A traditional EBITDA acquisition multiple is probably more appropriate given where Revelyst is at in its journey.

Government Approval

One other point that MNC Capital makes in their latest letter is that their offer isn’t contingent on approval from the government because it keeps the ammo businesses in a US business. That’s a good argument to shareholders, even though Vista is confident they’ll receive approval.

MNC is proud to represent an American alternative. Our proposal provides compelling value and certainty for Vista shareholders and is in the best interests of Vista’s employees and the broader safety and security of the U.S. We have confidence in the management of both the Kinetic Group and Revelyst and expect to work closely with them to achieve the full potential of both companies

Mark Gottfredson, Managing Director of MNC Capital

I don’t want to dive too much into that though because I don’t follow that side of their business or that industry in general. I’m mainly looking at the overall transaction on the implication for Camp Chef and the other outdoor lifestyle brands.