{kind=link}

One of the biggest stories in the outdoor cooking world over the past few years was Weber going public, hitting problems coming out of the pandemic, resulting in them going private again. It all happened in the span of a couple years.

As we’ve discussed in previous articles on the subject, the process of going private revealed quite a bit about Weber’s business. In our final article on the process documents created by the bank advising Weber, Centerview Partners, we’ll look at why we think it was going private or bust for Weber.

Weber Was Running Out of Money

Prior to going private, Weber took on $60 million in debt from BDT Capital (the company that took them private) and then another facility that totaled $350 million. The $350 million facility is notable because it came with a 15% interest rate and a 2% upfront fee.

Weber expressed that because sales were so poor through the grilling season, they didn’t have enough money to make it through the winter. That led to the debt, but even before the massive loan, BDT Capital noted in their acquisition offer that Weber’s

OUR PROPOSAL OFFERS IMMEDIATE LIQUIDITY TO THE COMPANY’S PUBLIC STOCKHOLDERS, WHILE ELIMINATING THE RISKS TO THE PUBLIC STOCKHOLDERS IN THE CURRENT MARKET AND OPERATING ENVIRONMENT THAT THE COMPANY’S CURRENT LEVERAGE POSITION IS UNSUSTAINABLE AND THAT THE COMPANY MAY BE UNABLE TO EFFECT A RECAPITALIZATION.

BDT Capital Partners

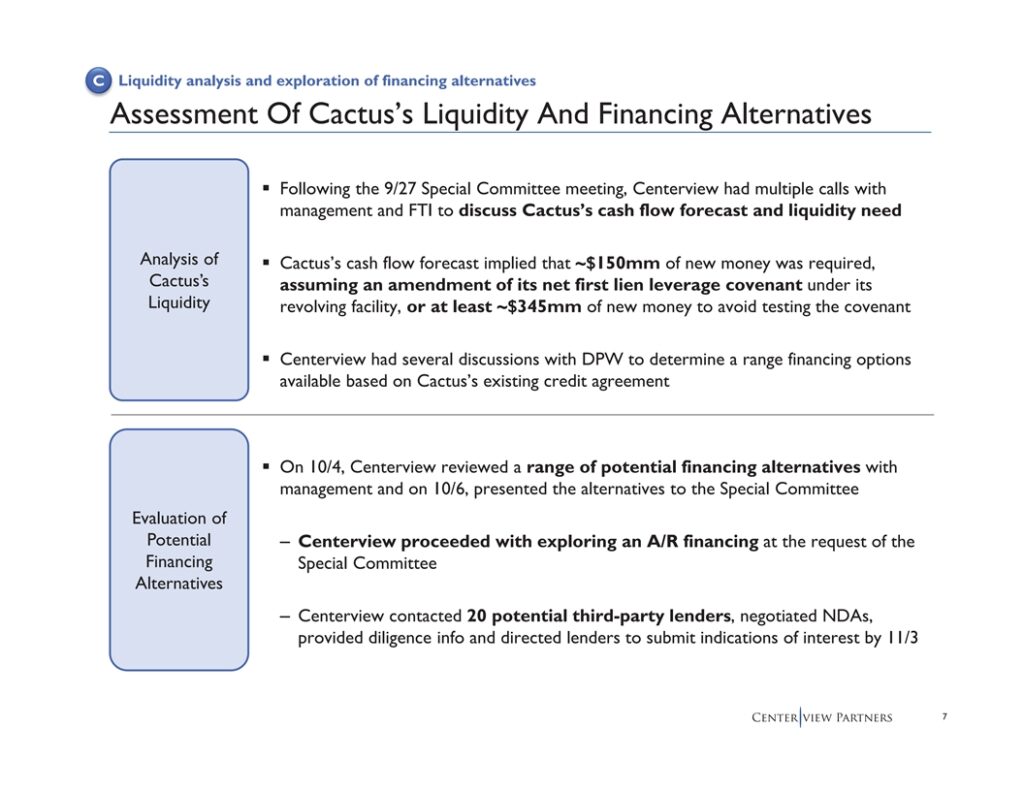

We can see from the liquidity forecast revealed in Weber’s SEC filings the magnitude at which Weber was running out of money.

As Traeger also noted in their most recent earnings, there is a cash trough at the end of March. The low point of cash happens because it’s the end of winter and sales haven’t started picking-up yet for the grilling season.

You can see from Weber’s liquidity forecast that at the end of March, if they didn’t alter their course last fall, their business would be short $128 million. It’s worth noting that the name “Bonsai” on the slide is a codename for BDT Capital and “Cactus” means Weber.

Debt Covenant Problems

When you take a loan out as a business, there’s usually debt covenants attached to it. They set financial ratios that a business has to hit, or else the business defaults. An example would be a ratio of earnings to total debt. The bank can remedy non-compliance with a number of different ways, including forcing liquidation, or requiring capital to be put into the business.

As part of compliance for a loan, a business will provide a calculation of the set financial ratios to the bank quarterly. Weber had a problem, that they would fail covenant testing with the path they were on.

From the liquidity forecast, it shows that Weber needed $128 million to have $0 left. That’s not the end of the money they needed because to avoid testing their covenants they needed at $345 million.

An important detail when Weber did end up amending their covenants with the bank is the amendment was contingent on being taken private.

Accounting Opinion

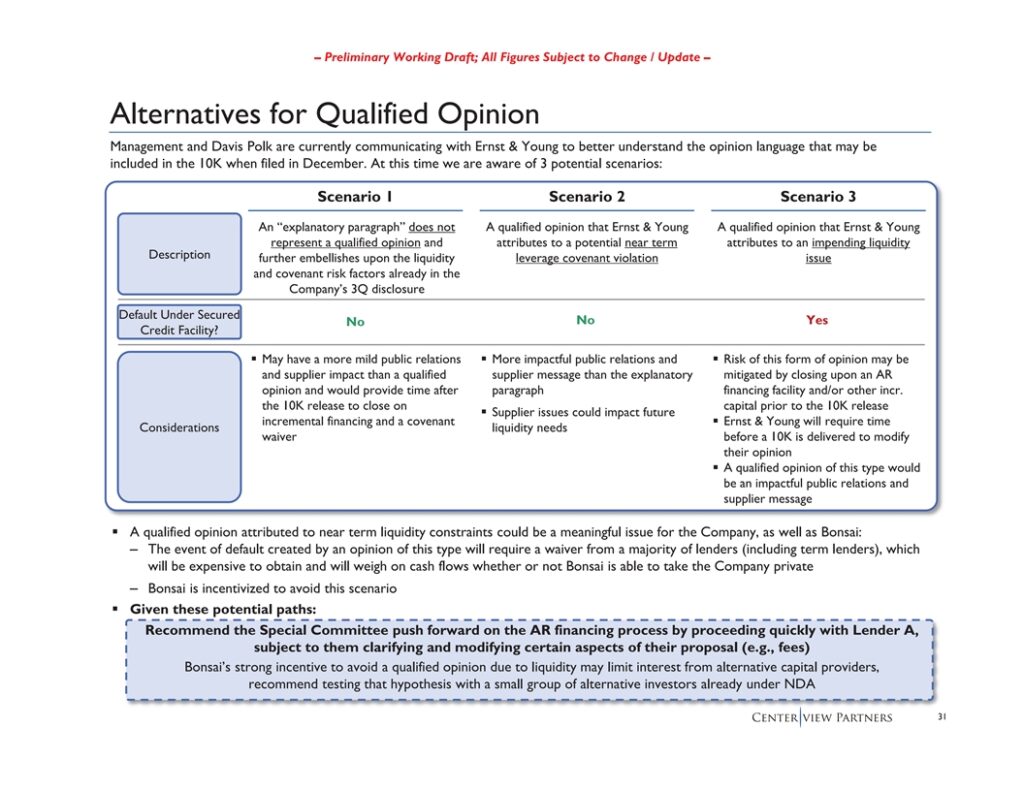

Beyond needing cash for operations and to avoid violating their credit agreement, Weber was also contending with the opinion language in their financial filings with the SEC. When financials are audited by an accounting firm, they include an opinion from auditors on the financial condition of the company.

The opinion from the accounting firm Weber used, Ernst & Young, was an area of concern for them. As you can see in the slide above, they were afraid that Ernst & Young would say they had an “impending liquidity issue”.

That would cause a cascade of problems, starting with another covenant compliance issue. They were also worried about the public perception and issues with suppliers if it was deemed that they had liquidity problems.

Weber Needed to Go Private

From looking at the information, it seems that Weber had to go private to avoid an eventual bankruptcy. Their largest shareholder said they had unsustainable levels of debt before they took on a bunch of additional debt at a high interest rate.

If they didn’t receive capital from going private, the additional interest burden from their debt load would have been hard to escape. Plus, even to amend the covenants for the debt they had, the bank said they had to go private.

Looking Forward

As we noted on our article showing Weber’s financial forecast, they need a rebound over the next few years to dig out of this. While they released a couple good products this year with the Lumin and their griddle, they’re betting on releases in 2024 being big for them. Hopefully the leader in grilling can get back on track, and this is just a bump in the road for their storied history.